By Gale A. Kirking, CFA

Today I’d like to really dig in on the responsibility aspects of responsible investing. In my previous essay (fourth in this series), I wrote about the very important financial aspects. In the essay before that (third in the series), I had provided some guidance to would-be responsible investors who need to decide what are those things that they really do want to support in their investing and, conversely, those things against which they aim to discriminate.

Now, that word “discriminate” carries all sorts of negative connotations, but, when it comes to serious responsible investing, it is exactly the right word for us. Discriminate describes precisely what we want to do. By definition, to discriminate is to

- exclude or treat differently than others some identifiable individual or group (human or nonhuman) while perhaps doing so in an adverse manner;

- make a distinction (or distinctions); and/or

- use good judgment.

A serious responsible investor is a discriminating investor. He or she says, “No, I do not want to see my money used to support that industry or business or cause or whatever, and, if there is no practical way to avoid doing so entirely, I will try as I can to minimize the extent to which my investments serve that activity.” The responsible investor may wish to discriminate against fossil fuels, gambling, pork products, abortion – whatever he or she chooses. The investor may want to support workers unionization and companies that have strong diversity, equity, and inclusion efforts, or he or she may want to oppose unions and DEI. “Socially responsible” means different things to different people, but this always involves discriminating.

In my opinion, responsible discrimination in the investment sphere has potential to change the world for the better. Many responsible investors, for example, are opposed to the continuing use and development of fossil fuels because burning coal, gas, and oil is the main contributor to global warming. If millions of individual and institutional investors refuse to own shares in, or bonds supporting, such businesses, those firms will need to look elsewhere for their funding, such as to banks. If the same investors refuse to invest or deposit their money in banks that support fossil fuels businesses, then that funding, too, will become scarcer. And if those investors put their money into companies making alternative energy sources more efficient and accessible, they will discriminate simultaneously – and positively – in support of alternative energy and, thereby, against fossil fuels.

This article is going to be all about how most effectively to discriminate in such ways while still earning good investment returns and acceptably diversifying one’s investment portfolio. Specifically, I will outline as an example a four-stage approach that I use in selecting responsible investments. Then, I will apply that example while walking through two real responsibility analyses of actual companies that I am considering for investment. Finally, I will build upon the presented information and process relating to individual stocks to discuss selection of collective investment instruments (most typically mutual funds and exchange-traded funds) as responsible investments.

The challenges of discrimination

There are different levels, or degrees, of responsible investing. That means different extents of discrimination (in all three of those meanings as defined above). I alluded to this in my previous essay. To generalize, I can say that stronger discrimination might make investing more difficult, more time-consuming, and perhaps (but not necessarily) less generously remunerative.

Continuing with the fossil fuels example, it is relatively easy to avoid investing in companies that engage in fossil fuels exploration, extraction, processing, and wholesaling. It is not too much more difficult to exclude from one’s investments the major oilfield services companies that support those industries. But, to go beyond that, things get trickier. Does one want to exclude also gasoline retailers, for instance, and any company that provides other inputs to the fossil fuels industry? To take my own investments as an example, I am quite strictly discriminating when it comes to fossil fuels, but

- I am invested in a grocery store chain that I like very much for, among other reasons, its efforts to reduce food waste and support feeding programs for the poor. It also retails motor fuels at some of its stores.

- I am invested in a water utility company that, I believe, is doing a lot to improve municipal water supply and sewer services across the U.S. There is another utility company that I have long avoided because it also provides large amounts of water to the natural gas fracking industry. Recently, the first water utility acquired (merged with) the second. So now what do I do?

- I am invested in an environmental engineering company that does a lot of excellent work to reduce pollution, support biodiversity, conserve water resources, and other good things. It also contracts with oil & gas and coal mining companies to mitigate environmental damage from their operations and implement post-mining land reclamation. Are these activities not also good things? Should I not support them with my investing?

There are two points that I want to make here while considering the examples I’ve given above: 1) The more strictly we discriminate, the fewer investment choices we have. Fewer investment choices might mean accepting smaller investment returns and less diversification to reduce risk. 2) Smart responsible investing requires making informed, reasoned, and intelligent choices. In my opinion and experience, it is also a subjective process that needs to be conducted according to well-intentioned guidelines but not solely by hard and fast rules.

What works well for me

Recognizing the two points described above, I have designed a responsible investment process that works well for me and that is acceptable to the partners (friends and family) with whom I invest. In our investing, I aim to achieve what I call “superior socially responsible, risk-adjusted return” through a thematic investment approach. Now, you may well ask, what is the meaning of all those fancy words strung together? I’ll explain it first at a high level and then in detail at the process level. Let’s focus on the terms “socially responsible,” “risk adjusted,” and “thematic investment.”

To repeat what I have said in earlier essays, the S&P 500, which in total market capitalization (or value) constitutes about 80% of the U.S. stock market, is wholly agnostic with regard to social and environmental responsibility. The biggest U.S. companies are included into the index pretty much by default. There are certain criteria for inclusion, but responsibility is not one of them. Companies in the index can do business in fossil fuels, weaponry, tobacco products, gambling, pornography, data centers, cannabis, abortion clinics, or just about anything else. The index does not discriminate. They can treat their employees, customers, and suppliers badly or well. The index doesn’t care. The companies can pollute, support tyrannical dictators, pay bribes, stretch the limits of the law, enrich their corporate insiders at the expense of other shareholders – or not. These matters are of no concern to the index.

Investment advisers may tell you that you have to invest into the whole market, or at least into the S&P 500, in order to achieve good returns and diversification at low costs. My answer to that is, no I don’t and you don’t either. You and I can invest into what we want to invest into – assuming we can figure out a reasonable way to do so. In my case, for instance, I do not invest into any company – no matter how profitable or popular – if I regard it to be behaving in a demonstrably and substantially irresponsible way. That rules out a large proportion of the S&P 500. So, I’m working within a select realm of acceptably socially responsible companies, and I have to achieve what investment returns I can within that domain.

But I discriminate even harder, because I invest into only 6 sectors (and according to specific investment themes within each) that I have personally defined, understand very well, and believe are of special importance. Any company that does not fall into one of those sectors doesn’t get into the portfolio. My personal sectors include 1) Life sciences and biotechnology; 2) Environmental management; 3) Food, agriculture, and aquaculture; 4) Health care services; 5) Medical technology; and 6) Water resources. I have special knowledge in these sectors and have been investing in them exclusively for about 10 years. You may notice that there are a certain amount of overlap and some common characteristics with regard to life’s necessities across this group. That’s the thematic investment aspect. (Actually, in 2026, I am adding to our investment universe 4 additional sectors that stray not far from the existing themes.)

Thematic investing reduces the breadth of my investment universe. I can make up for this to a certain extent by diversifying across firm sizes (small, medium, and large) and geographies. This also motivates me to focus very closely on what I am buying and not buying. I imagine this is something like being a vegetarian (which I am not). If one doesn’t eat meat, then he or she needs to look around at other protein sources to make sure of getting the proper balance of amino acids (the building blocks of proteins) from other high-quality sources.

I am not recommending these sectors – or even my approach as a whole – to anybody. I am describing as a real-life example just one approach to responsible investing that fits my world view, knowledge and skill set, and moral framework. Your world view, knowledge and skill set, and moral framework most certainly are different from mine. Moreover, as I described in my previous essay, if an investor wants to be discriminatory, he or she need not do that with the entire portfolio.

What are socially responsible, risk-adjusted returns?

Investment theory and practice recognize that reducing and managing risk is valuable and that high expected return should not be the sole objective. As noted above, I aim to achieve superior returns, but these are returns of a specific type. They are socially responsible and risk adjusted. The S&P 500 as a whole is only capable of delivering responsibility-agnostic returns, as I have described. By my being choosy about what companies go into our portfolio, we earn investment returns less soiled or tainted by irresponsible activities. Arguably, too, our portfolio is more conservative and less risky than is the S&P 500 as a whole. That risk profile suggests our portfolio may sometimes underperform purely in financial terms when markets are rising but outperform when markets are falling, and the returns data have generally borne that out. Rather than to wander further off into the weeds on financial theory, however, I’m going to move on.

What do we mean responsible?

Before I describe the four-stage framework that I personally use in evaluating and selecting companies as potential investments, I want to digress briefly concerning terminology. I have been using the word “responsible” as an umbrella term to embrace a whole host of descriptors – all with similar but not necessarily identical meanings. In investing, we can encounter such terms as

- Sustainable investing and sustainability;

- Socially responsible investing (SRI) and corporate social responsibility (or “CSR”);

- Ethical investing;

- Environmental, social, and governance and ESG investing;

- Impact investing;

- Morally responsible investing;

- Green investing; as well as

- Faith-based, values-based, or Catholic values-based investing.

Even the list above is not comprehensive, and the financial services industry, among others, continues to come up with new terms. Moreover, a given descriptor might mean one thing to one person or marketing team and something different to somebody else. The one thing they have in common is that all refer to discriminating investments as I defined that term at the top of this essay. The specifics of responsibility are in the eyes of the beholder, the marketing people, and the investor.

In my experience, “corporate social responsibility,” or “CSR” for short, is the oldest of these terms. I first encountered it in the early 2000s, when companies were beginning to describe their CSR credentials and activities in their annual reports and, soon thereafter, in wholly separate CSR reports. (In my work, I should note, I assist some of those companies in producing their reports.) Together with “responsibility” as an umbrella term, I prefer to use the abbreviation “CSR,” and for two reasons: 1) because that is an expression I’ve been using for more than 20 years, and 2) I think environmental and social responsibility are largely one and the same. What’s good for the environment within which we live is also good for society, and I like to broaden the term “society” to include all living things and ecosystems.

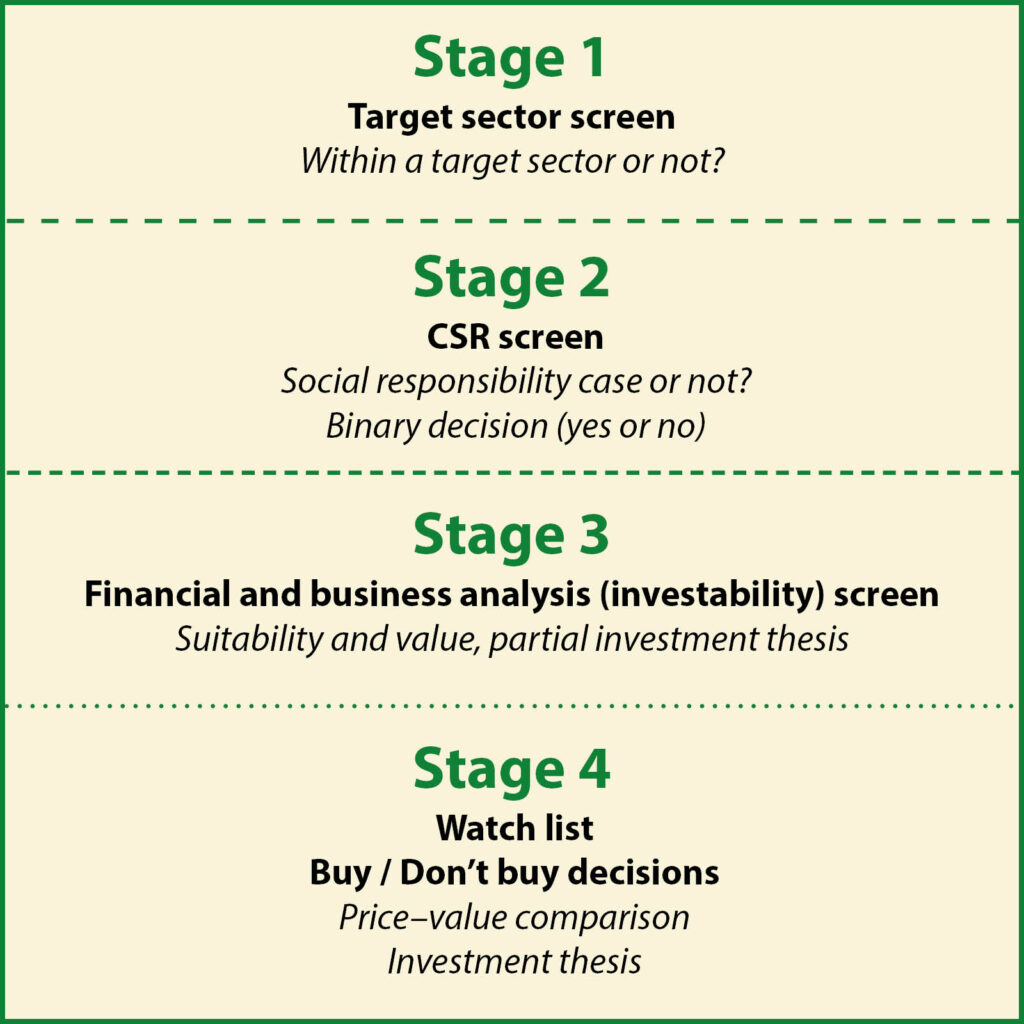

My four-stage process

As mentioned in an earlier essay in this series, I personally aim to separate what I call the “CSR” aspects of investment decision-making from those involving financial and business analysis and buy or don’t buy decisions. In the four-stage approach described below, the CSR decision is reached in stages #1 and #2. The figure below depicts those stages, each of which ends in a decision.

A four-stage approach to responsible investment decision-making

Stage 1: Does the potential investment fit into one of my target sectors?

My first step simplifies things a lot right from the start. As I’ve noted, I invest into only 6 sectors of my own definition (expanding to 10 in 2026). If a company doesn’t fit into one of those sectors, I’m not going to give it a minute’s consideration. To see how that streamlines matters, let’s look, for example, at the first 20 companies from the S&P 500, as arranged alphabetically (below).

Alphabetical partial list of the S&P 500 companies

| S&P 500 constituent | Within a target sector |

| Abbott Laboratories | Yes |

| Accenture | No |

| Adobe | No |

| Advanced Micro Devices | No |

| Aflac | No |

| Air Products and Chemicals | No |

| Allstate | No |

| Bank of America | No |

| Berkshire Hathaway | No |

| Boeing | No |

| Broadcom | No |

| Bristol-Myers Squibb | Yes |

| Caterpillar | No |

| Chevron | No |

| Cisco Systems | No |

| Coca-Cola | No |

| Comcast | No |

| Danaher | Yes |

| Disney | No |

| Dow Chemical | No |

Only 3 of these 20 (15%) would possibly be of interest to me, because they fall into sectors within which I invest. Coincidentally, by the way, 2 of these companies are in fact in our portfolio. Danaher, a life sciences company, has been there for a long time. Bristol-Meyers Squibb is also in the portfolio, but new purchase of its shares has been suspended on fiduciary and social responsibility grounds since 2021, when it was reported that the company had been using a dodgy tax avoidance scheme, which I judged to be not responsible.

Because of this high-level sectoral discrimination, I don’t need to ask myself if I should consider, for instance, investing in a major oil company, like Chevron, or a purveyor of sugary drinks, like Coca-Cola, or one of the world’s largest producers of plastics, Dow Chemical. Something like 85% of the overall stock market simply lies outside my potential investment universe. My first screen of potential investments is very simple and rule-based.

Stage 2: The CSR screen

The next screen is not so simple. It is more subjective, judgment-based, time-consuming, and directed by guidelines and principles more than by rules. Nevertheless, my aim is to reach a binary decision: either, yes, this company satisfies my CSR criteria (broadly defined) or no, it does not satisfy the criteria. If the answer is yes, then the potential investment may move to step 3. If the answer is no, the potential investment is excluded. Sometimes, a no decision becomes quickly apparent, but very frequently a lot of research and consideration is needed before making the binary decision.

So, on what basis am I making these judgments? As I described in the third essay within this series, I take what can be called a “stakeholders” view. The major stakeholders whose interests I consider are the following:

- Investors,

- Climate and environment,

- Customers,

- Employees,

- Communities and society, and

- Suppliers.

Shortly I will discuss these stakeholder-interest categories individually using a real-world example, but suffice it to say at this point that I will be digging to find out how the company or other investment vehicle treats these stakeholders and respects their fair interests. Very commonly a given company will be strong in some points, weaker in others, and I give credit where credit is due. For example, a company may be very small but developing a promising potential new drug for a devastating disease. It may not show much interest in climate change or the community where it operates, but it treats employees and shareholders well. Based upon the information I can acquire, if I can formulate a reasonable social responsibility case (a “CSR case,” as I call it) to justify potentially investing in the company, it will be able to clear this screen.

Stage 3: Financial and business analysis

The fact is that, in many instances, by the time I get done looking at a company in Stage 2, I already will know enough about that company to determine that it is not going to get to Stage 3 even though it may have a strong CSR case. That is because I can already see that it is not going to pass muster in one or more financial aspects, that its business model or competitive position is not investment-worthy, or that one or more risks associated with the company are simply unacceptable. Maybe its debt is too great and/or profitability too low, perhaps it is facing serious litigation challenges, or possibly its growth prospects are too weak or management team seemingly untrustworthy.

In any case, first screening out those companies that do not satisfy my sector and CSR criteria makes me more efficient in my financial and business analyses, because I can focus my attention solely on companies that might seriously be of interest. In my next and final essay (number 6) in this series, I will discuss this stage of analysis very closely. Suffice it to say here, that this analysis will be directed to determining if what I call a “partial investment thesis” can be formulated for the specific company. If yes, that means that what I later will describe as the “fundamental determinants of value” for this potential investment make it attractive if the share price will also be right. Essentially, what I aim to determine here is what some will call the “intrinsic value” of the given company and its shares. I want to note that the CSR case and the investment thesis are separate things, but a company’s shares will be acquired only if both of these are satisfactory.

Stage 4: Is it attractive on a price:value basis?

If a company gets to stage 4, that means there is an investment thesis arguing that these shares should be in our portfolio – if I can find a way to get them there. “Finding a way,” then, is mostly about the share price. That investment thesis was partial back in stage 3, because it did not in and of itself consider what is the current share price in the market. Clearing screen 3 may only result in the stock being added to my “watch list,” a group of companies whose stocks I like. It’s like a wish list – if only I can justify spending the money. I’ve determined a fundamental or intrinsic value, but now I need to compare that to the actual price at which I can buy the shares.

So, let’s say I’ve determined a stock is worth $50, but it is currently priced by the market at $70. I may very much want to have the company’s stock in our portfolio, but I’ll only buy it if and when I can get it for ≤$50. This is my price:value comparison. I may wait months or even years to acquire shares in a company that appeals to me. The partial investment thesis that brought the stock to this stage becomes a complete investment thesis when and if the price comes down to $50.

Now, as a practical matter, stocks do not have intrinsic values that can be calculated to nice round numbers like $50. It’s more like “around $50” or in the $47–$51 range. In this hypothetical case, I might begin buying when the share price comes down to about $52 and try to keep buying as it, hopefully, moves lower still. It is the average acquisition price of the stock position that matters.

Moreover, I will continue to monitor the companies on my watch list, because the fundamental determinants of value change through time. My understanding of the existing fundamentals and the relationships among them may also shift. I’ll have a lot more to say on that in my final essay.

Obviously, the process I have outlined is one of sifting and winnowing, so to speak, separating the investable kernels from the unappealing chaff. Just approximating, I’d say for every 20 stocks that get to stage 2 not more than 2 or 3 will make it as far as stage 4 and maybe 1 will ultimately get into the portfolio.

What about steps 5 and 6?

I generally aim to be a buy-and-hold investor. That means I put a lot of effort into doing the research and analysis up front before I invest, thereby, hopefully, reducing the probability of making a buy decision that I later regret and need to reverse. Nevertheless, the investment process does not end with a buy decision in Stage 4. One might say that Stage 5 is to monitor the existing portfolio and its individual components on an ongoing basis. Someday I may need to sell out an individual position as conditions change or the overall balance of the portfolio across sectors might get out of whack and need adjusting. I should monitor price development and returns performance, too, in order to evaluate whether or not my investment approach and philosophy are actually working as I have imagined that they should.

Ideally, there is yet another aspect, let’s call it Stage 6 (although it would actually overlap with Stage 5). This is stewardship and engagement with the managements of the companies in the portfolio, as well as, perhaps, interaction with other shareholders. This also involves voting at the annual meetings but can go far beyond that. Stewardship and engagement might be directed primarily to protecting shareholder interests, but it is also a way to encourage companies and their managements to behave responsibly in other ways. This is exemplified, for example, by work of the Interfaith Center on Corporate Responsibility (www.iccr.org), an alliance of religious and investor groups that has been active in this area for more than 5 decades and speaks for more than $4 trillion in investment assets. ICCR started out opposing apartheid in South Africa during the 1970s while pressuring companies to divest their investments there. Today, ICCR leverages its influence on issues related to climate change, worker justice, health care equity, and others. ICCR is big and influential, but, as a practical matter, it is difficult for individual investors to have much influence in this manner.

Applying the process: GE HealthCare and CareDx as examples

Now, to provide true-to-life examples, I want to look at two specific companies that as of this writing are subjects of my Stage 2 CSR evaluation. Due to space limitations, I obviously won’t be able to go into all the detail here, but I will give you the general flavor and methodology in practice. The two companies under consideration are GE HealthCare Technologies (stock ticker GEHC, website www.gehealthcare.com) and CareDx (CDNA, www.caredx.com). I will refer to them hereafter by their tickers.

GEHC and CDNA easily clear my first screen, because each company has one foot in the medical technology segment and another in the health care services segment. GEHC works in medical imaging, diagnostic products and services, and various other medical devices, products, and services. It was spun out of the large U.S. conglomerate General Electric (GE) in 2023 to become an independent company. CDNA discovers, develops, and commercializes diagnostic solutions specifically focused on organ transplantation and taking in the entire transplantation journey, from pre-transplant to peri- and post-transplant. GEHC is roughly 100 times larger than CDNA and has a corporate history dating back more than 125 years. CDNA was founded in 1998.

Both companies are working to extend and improve lives, so they come into the CSR evaluation with positive starting credentials. Now I need to evaluate how each stacks up in terms of its attitudes, actions, and actual performance relative to the interests of their stakeholders consisting of investors, climate and environment, customers (including patients), employees, communities and society, and suppliers. I am going to have stricter expectations for the larger, better-resourced, and older GEHC than I will of CDNA. I closely follow the sectors within which both companies operate. GEHC became potentially interesting for me a couple years back, only when it was spun out of the mammoth GE conglomerate to become a pure-play health sector company. CDNA is completely new to me. I started looking at it when CDNA entered into a partnership with another company in which we already own shares.

Getting started…

Here are some of the first things I’m going to do as I undertake this process, and more or less in this order:

- Create a separate subdirectory on my computer for each company.

- Create an MS WORD file within each subdirectory (e.g., called “Notes on GE HealthCare”) for collecting my notes, observations, and analysis on each. I do this for every company I look at, and I almost never delete anything. Each time I come back to look at a company, I add a date at the top of the text file and begin recording my new notes there.

- Visit and peruse each company’s website. I’ll look especially at GEHC’s “Sustainability” and “Investor Relations” pages, but there also are sections about “Our Economic Impact,” “Suppliers,” “Community Engagement,” the GE HealthCare “Foundation,” and more. At CDNA’s website, there are sections called “Compliance & Ethics,” “Corporate Responsibility” and, again, much more albeit unsurprisingly not so much as in GEHC’s case.

- Download and study each company’s latest CSR report (termed the “Environmental, Social, and Governance Report” at CDNA and “Sustainability Report” at GEHC).

- Download and skim the latest 10-K (i.e., annual) report of each company. This will be more important if we get so far as Stage 3, the financial and business analysis, but still, it is worthwhile to take a quick look at it now.

- Take a quick look at quarterly reports, press releases, and other materials issued by the company. All of these are on their websites.

Assessing quality of CSR reporting

In the course of doing what I have described above, I am already assembling and working through quite a large amount of information and yet I’m just getting started. GEHC, in particular, like most big companies, produces a lot of documents – mostly glossy, colorful, with lots of pictures and graphics, and texts glowing with self-praise. Big public companies typically have whole teams of spin-doctors working on this stuff, so we need to absorb all this with a grain or two of salt. I am looking for what each company reports – or that I can discover – that is relevant in relation to the stakeholders of interest. In addition to data and facts, I am keen to sense how much of it is real and substantial, how much of it is outright greenwashing, and even how much of it is pure puffery (i.e., nice, but not really relevant to the CSR evaluation). The probability that these materials contain a mix of real substance, greenwashing, and puffery in some proportions is basically 100%.

For assessing the quality of CSR reporting, each company’s CSR report is only a starting place and other parts of the website and company documents, too, contribute to that reporting. CDNA’s Environmental, Social, and Governance Report is 34 pages long. GEHC’s Sustainability Report has 86 pages and is a lot more impressive to look at. Bigger, glossier, and more colorful are not necessarily better. We are interested in appropriate and useful content that explains what is actually going on in the company and its business.

A good CSR report (regardless of what title it is given) should specify which stakeholders the company regards as important. It should set out priorities, policies, and goals. It should spell out a framework for self-evaluation, as well as processes for achieving the stated goals and scales for measuring progress toward those goals. The report also should provide real evidence of its progress.

Both CDNA and GEHC have pretty good CSR reports. I suggest you pop open the .pdfs from the websites and take a look at them. (I’m working with the 2024 versions of these documents.)

GEHC’s report, in particular, is supplemented by several additional, separate documents and more materials on the website. One major such document is entitled “The Spirit & The Letter” and is a 45-page publication detailing the company’s “Code of Ethics & Integrity.” This is quite important for GEHC because, as we shall see shortly, the company faces some reputational issues in this area. In the introduction to the code, the CEO declares: “The essential message is simple: we always act with the highest integrity. We do not tolerate illegal or unethical behavior.” This is a bold pledge, and especially so for a company that has had some challenges in this area, so GEHC’s management darn well better prove that it is serious about this. Other of its additional documents include a human rights policy and information sheets on the controversial areas of animal research and stem cell research.

In the responsible investing world, there exist a number of formal and recognized frameworks for guiding, tracking, and demonstrating CSR progress. CDNA uses the internationally recognized Global Reporting Initiative (GRI) standards. GEHC goes farther. The appendices to its Sustainability Report begin with its own key performance indicators (KPIs) covering a range of topics (e.g., environmental performances, workplace safety, compliance and ethics). Then, it provides information according to the Sustainability Accounting Standards Board (SASB) metrics, as well as climate disclosures inspired by the Task Force on Climate-Related Financial Disclosures (TCFD) framework. Both companies provide statements regarding their greenhouse gas emissions issued or verified by an independent certification agency. GEHC includes a discussion of its contribution to achieving 12 of the 17 United Nations Sustainable Development Goals (SDGs). CDNA mentions 8 of the SDGs with which its “sustainability/ESG initiatives intersect.”

I like to look for special issues potentially of CSR significance. I note that GEHC’s CEO was during 2024 and 2025 chairman of AdvaMed, a well-funded and powerful lobbying organization representing medical device companies in Washington, DC. I would not say this is a red flag, but it nevertheless is a flag and calls for further examination. AdvaMed sometimes lobbies against existing and proposed regulations that might be considered beneficial to patients and the environment. Potentially on the positive side, in 2024, GEHC established a foundation through which it financially supports nonprofits working to improve health care access, especially maternal health care and in poor African countries.

Based upon my review of their internal documents (and I’ve only touched upon highlights here), both CDNA and GEHC demonstrate serious approaches and attention to CSR matters. GEHC is investing a lot more into all of this than is CDNA, but that is to be expected. For its size and possibilities, CDNA looks pretty good on paper, as it were, too.

Moving from internal to external information

In conducting a CSR assessment, I evaluate data and information that can be classified in three ways according to how much control and influence the companies themselves have over the materials:

- those over which the companies themselves have complete control, as in the published materials just now discussed above;

- those over which management has influence (and possibly considerable influence); and

- those over which company management has only indirect influence, for example by their actual behaviors and actions and the behaviors and actions of their colleagues within the firm.

CSR ratings and certain public recognitions fall into the second category. The third category includes things like media coverage in cases of controversy as well as online independent ratings of those organizations as places to work.

In category two, we might note that GEHC was named by Fortune magazine as one of the World’s Most Admired Companies for 2025 (ranked 6 out of 15 among medical products companies). This, according to Fortune, is based on an “annual survey of corporate reputation.” That is to say, this is corporate managers opining on other corporate managers. This is a nice tribute, but it tells us nothing about CSR. GEHC also was awarded the EcoVadis Silver Medal in 2025, and this is meaningful in CSR terms. We nevertheless should be aware that the award is based upon GEHC’s own efforts and paid participation, which means it decided to compete; completed a questionnaire to evaluate the four areas Environment, Labor & Human Rights, Ethics, and Sustainable Procurement; and then documented its efforts to improve.

The trophy collectors

Some public companies are trophy collectors, seemingly constantly on the lookout for awards competitions within which they can participate. Neither GEHC nor CDNA appear to be trophy collectors. A good example, though, might be seen in the French electrical and electronic equipment provider Schneider Electric. Some of Schneider’s recent awards are shown below. It is not a bad thing for a company to hoard recognitions, but the responsible investor needs to understand what are the underlying reality and importance of those trophies. Some of them are really meaningful, although it may not be superficially clear what is their actual significance, while others may essentially be purchased greenwashing.

Example: A view into a corporate responsibility trophy case

| Some of Schneider Electric’s Responsibility awards from 2024 | |

|

|

Schneider Electric’s trophy case provides a small sampling of organizations that produce and/or gather CSR/ESG/sustainability ratings. Dozens of these are in existence. Although these outfits typically present themselves as objective and deeply analytical evaluators, many of them, in my opinion, have ratings systems that are easily manipulated by the companies being rated or are overly generous in ranking friendly (sometimes paying) companies. For example, a media company may be more likely to give an award to an actual or potential advertiser. Awards given by a trade association are more likely to go to members of that association than to their peer firms in the same industry that have not joined the association. The point is that if you are using such information, you need to know what is behind the award.

In the table below, I am presenting as examples just four such rating organizations and their numerical scores for GEHC and CDNA as well as for Philip Morris, whose many tobacco and smokeless nicotine products include, for example, the Marlboro brand. The best score in each case is shown in bold. I’m including Philip Morris to illustrate a specific point.

A CSR ratings sampler

| Responsibility metric | GEHC | CDNA | Philip Morris |

| CSRHUB (0–100, 100 being best) | High 87 points with 36 sources | Low 26 points with 19 sources | Very high 95 points with 57 sources |

| Morningstar Sustainalytics ESG risk rating (0–100, 0 being best, “severe” risk being 40+) | low-risk 16.97 | high-risk 32.76 | Low-risk 17.16 |

| ISS Governance QualityScore (1–10, 1 being best) | 4 | 5 | 2 |

| S&P Global ESG Score (0–100, 100 being best) | 50 | Not freely available | 78 |

I will explain these metrics only briefly. CSRHUB is a Certified B Corporation that provides aggregated ESG/CSR/sustainability ratings for thousands of companies. It collects data from hundreds of sources. I think its intentions are good. Big companies like GEHC and Philip Morris are rated on the basis of dozens of available sources, many or most of which they themselves provide or influence (categories 1 and 2 as described above) and appear to me to achieve higher ratings. Smaller companies, like CDNA, are rated on the basis of few sources. Morningstar Sustainalytics examines so-called ESG-related financial risks. In my second essay in this series, I discussed why I personally believe that ESG-related financial risk is not a very useful concept. The ISS Governance QualityScore is produced by Institutional Shareholder Services, a so-called proxy advisory firm that guides investment funds and institutional investors about how well corporate managements are doing in running the companies into which they invest and how to vote on shareholder resolutions. The S&P Global ESG Score compares individual companies with their peers in their same industries. It typically is used in creating and managing large ESG investment funds on a best-in-class basis. I discussed best in class in my second and third essays in this series, as well as why I personally do not hold best-in-class approaches in high regard.

I won’t tell you, the reader, what to regard as responsible or irresponsible, but the fact that the Marlboro Man corrals 3 out of the 4 highest scores shown in the table may indicate that no single number in isolation provides a flawless and comprehensive representation of a responsible company.

Muckraking, dirty laundry, and praiseworthy deeds

Let’s now move into our search for category 3 information, that over which company management has the least influence. Now we are basically digging into the world wide web, and this, if we are lucky, will turn up a nice mish-mash of material for us to comb through. Probably some of it will flatter the subject company, but this is also how we identify actual and potential problems and see how some of the rest of the world views the company.

I’ll start out with an easy pitch, querying in Google “Is (company name) a socially and environmentally responsible company?” Here are the first couple sentences that Google’s AI Overview offers in response to this query:

“GE HealthCare has established itself as a company with a strong focus on environmental, social, and governance (ESG) principles, particularly since becoming an independent company in 2023. The company integrates sustainability into its core operations, aiming to achieve net-zero emissions by 2050 and focusing on expanding healthcare access.”

“CareDx, Inc. positions itself as a socially and environmentally responsible company, primarily focusing its Environmental, Social, and Governance (ESG) efforts on improving the transplant patient ecosystem. The company has formalized its commitment through an ESG framework, an annual ESG report, and initiatives aimed at health equity, diversity, and environmental sustainability.”

Now, I do not disagree with these characterizations, but neither would I take them at face value. A deeper AI search comes up with much, much more about both companies on many aspects of environmental, social, and governance responsibility. Almost all of it is very positive and mostly drawing upon the companies’ own publicly available information that we have already obtained from their websites.

So, let’s query a little more aggressively, asking “What is the controversy surrounding (name of company)?” This is an excellent and usually quite productive general query. Maybe there is no controversy at either GEHC or CDNA, but, if there is anything out there at all, it’s likely to show up here. One thing to bear in mind is that any big company that has been around for a while will face some issues. Moreover, any internet search, and perhaps especially any artificial intelligence-driven search, can come up with some things that are partly or even wholly false or misleading, so it is appropriate to be cautiously skeptical and to probe deeper.

Again, Google’s AI responds as follows (showing just the first few sentences):

“The controversies surrounding GE HealthCare in recent years have primarily focused on potential foreign bribery investigations in China, serious product safety recalls, and, more recently, financial impacts from international trade tensions and supply chain limitations. As of late 2025, the company has cleared major regulatory investigations but faces ongoing pressure from new trade tariffs and complex, high-stakes litigation involving allegations of aiding extremist activities in Iraq.”

Oof! The response goes on to detail “tender irregularities” and “allegations of bribing Chinese government and hospital officials to sell medical equipment…After a seven-year investigation initiated in 2018, the DOJ and SEC informed GE HealthCare in May 2025 that they were closing their investigations with no further action taken, as reported in the company's 10-Q filing.”

And…

“The controversy surrounding CareDx, a diagnostics company focused on organ transplant patients, primarily centers on federal investigations into its business practices, accusations of securities fraud, and intense legal battles with competitors over patents and advertising.”

Hmm… The response goes on to list government investigations relating to possible false advertising, inducements paid to physicians to use the company’s products, and a class action lawsuit over its reporting to shareholders. Also mentioned are legal battles with a competitor (Natera) over intellectual property rights, and reports of high employee turnover.

Whew! Kinda scathing, but it is important to dig in further. CareDx has in the past been investigated by the U.S. Department of Justice relating to alleged improper Medicare billing and payment of inducements (kickbacks) to physicians. Ultimately, though, the government declined to prosecute and CareDx generally insists the accusations were without merit. That said, a certain cloud does hang over the company in this area and so management has its work cut out for it to rebuild reputation. A shareholder class action suit, meanwhile, claimed that by declining to report details of these investigations on a timely basis the company caused shareholders to lose money when the news became public and the share price dropped. The suit was settled with a $20 million payment, no admission of guilt, and a commitment to make specific and detailed reforms in the area of CareDx’s corporate governance practices. The company has a history of legal battles over intellectual property, which is not at all uncommon in its industry. For example, CareDx has had legal battles with Natera, and it may very well have them again in the future. In part, that seems to reflect that Natera is rather a big bully in this space and uses lawsuits to intimidate its competitors. Natera has itself been accused of transgressions similar to those it claims against its rivals.

Once again, I want to emphasize that this kind of research may initially raise more questions than it does answers, and that is just fine and useful. As demonstrated by the GEHC and CDNA cases, deeper investigation is almost always required to get to clear answers. Further to demonstrate this point, but also just out of curiosity, I ran this same query for Jesus Christ, whom many (not all) will regard as socially responsible. Google’s AI reports:

“The controversy surrounding Jesus Christ centers on his claim to divinity, his disruption of established religious laws, and debates regarding the accuracy of the Gospel narratives. Critics, historically and presently, debate his role as Messiah, his actions on the Sabbath, and his, at times, polarizing teachings.” It gets worse from there, as AI points out, for example, that Jews consider Jesus to be “a failed Messiah,” that “his views on eunuchry and celibacy were considered radical, and that some of his “contemporaries even considered him to be demon-possessed or insane.”

Other areas, briefly

I want to touch just briefly here on a couple more areas while emphasizing that a thorough CSR evaluation involves probing more deeply and in additional areas, depending upon what you as the responsible investor believe is most important.

While on the subject of internet searches, to examine how its employees view a given company, the following is a useful query “Is (company name) a good company to work for?” This likely will get you an AI Overview as well as commentaries from the likes of employer rating platforms such as Glassdoor and Indeed.

One of the first things I look at in a corporation is the content and qualifications of the board of directors and top management. If I read in the CSR report about the company’s commitment to diversity but see only white men sitting around the board table and in the C-suites, then I’m skeptical about how committed management really is to what it is telling us. This even can reflect on management’s credibility more broadly. Also, if the CEO’s executive assistant is pictured on the first row of photos in the annual report among the company’s managers, well, good for her, but she’s probably not there because she’s running the company. I have actually seen this sort of thing, by the way.

As an investor, I also want to see diversity of experience and strong qualifications on the board. I prefer to see a good representation of independent directors (i.e., who are not members of the management team or having family or other relationships to the company). I strongly prefer to see that the CEO is not also chairman of the board, because a combined CEO and chair concentrates too much power in one person (usually a man) and suggests that the board is a rubber stamp for the big guy at the top. In the U.S., these roles are combined in about half of public companies. The roles of CEO and board chair are separated at both GEHC and CDNA.

Pass or fail? Then what?

I have described here only a fraction of the work that my CSR evaluations entail, but I hope it has given you a general sense and flavor. Ultimately, both GEHC and CDNA pass through my CSR screen. A reasonable CSR case can be formulated for each (see text box). Neither is perfect on all CSR criteria, but few companies are (maybe none). Both are doing good things for society in their businesses, appear to be correcting for past shortcomings, are taking serious approaches to responsibility and sustainability, show strong commitments to the stakeholder interests that matter to me, and are making progress toward their goals. They move to my bin #3.

CSR cases for GEHC and CDNA

GE HealthCare Technologies is a medical device company whose business and research activities are solely devoted to the development, manufacture, and marketing of products, services, and complementary digital solutions used in the diagnosis, treatment, and monitoring of patients in the United States and internationally. It has a strong focus on the interests of shareholders and patients. The company appears to have sound frameworks and processes in place addressing responsibility and interests of relevant stakeholders. It is a big and complex company and still carries some ethical baggage from its days as part of the larger GE conglomerate. GEHC needs directly to face up to these issues. Viewed comprehensively, GEHC clears our CSR screen, albeit while coming into the business and financial analysis with business risks that will require further analysis.

CareDx is a pioneering firm in the important areas of transplantation and precision medicine. It operates in a brutally competitive and litigious industry that is also largely dependent upon government agencies and programs (e.g., Medicare) for its revenues. To a certain extent, controversy goes with the territory. Although it has not been found guilty of Medicare fraud or improper sales practices, these are issues which may not go away. This seems to me more about business risk, however, than it is a CSR issue. CDNA demonstrates a serious approach and attention to CSR matters but leaves considerable room for improvement here. Viewed comprehensively, CDNA clears our CSR screen.

Does this mean GEHC and CDNA shares will enter our portfolio tomorrow? Not at all. Remember that the CSR decision is a binary, yes–no screen, determining whether or not the candidate can move to Stage 3, which is the financial and business analysis. There, I will determine if these companies are investable in terms of their prospects for generating good investment returns with acceptable (low) levels of risk to those earnings streams. Just as I need to see a CSR case for the companies to clear Stage 2, there must be a reasonable to strong (partial) investment thesis to clear Stage 3, and most companies that get this far never make it to Stage 4, where the buy / don’t buy decisions are made on the basis of comparing intrinsic value and share price in the market.

Then, too, at Stage 4, a decision to buy will depend upon 1) if there is cash available to invest, 2) how attractive is the given company and its investment thesis compared to the alternative companies and investment theses also on the watch list, and 3) the diversification needs of the investment portfolio at a given point in time. More on that in my next essay.

CSR evaluation for collective investment vehicles

If screening and evaluating individual companies as potential investments seems like a lot of work, well, that’s because it is, at least if a person is going to go about it in a serious way. Alternatively, and as I have discussed previously, a responsible investor may choose to invest some or all of his or her investable funds into collective instruments, most likely mutual funds but maybe exchange-traded funds (ETFs). The social responsibility of a collective investment vehicle is in large measure the sum of its parts, those parts being the individual securities (companies) in the fund portfolio. Fortunately, the concepts discussed above are useful also in evaluating funds.

Unless a responsible investor is working for a large investment firm, he or she obviously is not going to be able realistically to evaluate every company whose shares are included in an investment fund. Very few such funds will have fewer than several dozen constituent holdings and, in most cases, these number in the hundreds. Portfolios with even more than 1,000 constituent positions are not unusual.

A higher-level view

From a practical viewpoint of time and work, therefore, we as individual investors need to take a higher-level view in evaluating investment funds on CSR criteria. I suggest that this means examining what companies and industries are included into the fund portfolio, what policies and stock selection procedures a given fund’s managers claim to follow, and how well do those managers practice what they claim.

One thing we must not do is to select what we hope will be responsible investments just according to the name given to a particular fund. Naming is about product creation and marketing, not investment management. That said, I will note there has been a little progress toward truth in advertising within this area in the European Union (not so much in the U.S.). With effect from 2025, the EU has a so-called “80% threshold rule” requiring that investment firms using terms like “green,” “ESG,” “sustainable,” or “climate” in the names of their investment products must allocate at least 80% of the underlying portfolio weight to assets meeting certain environmental or social characteristics. As a result of the new rules (which I regard as minimal and not at all severe), many European funds have now dropped the likes of “ESG” “Impact,” and “Sustainability” from their product names. I suspect there would be a similar shift in the U.S. if greenwashed naming were prohibited there.

For my own purposes, I rate investment funds in CSR terms on a scale from 0 to 10. I call this the Responsible Investing Continuum, and it ranges from “responsibility agnostic” (at 0 points) to “rigorously responsibility focused” (at 10 points).

Responsible Investing Continuum

Please note that 0 points and “responsibility agnostic” are not indicators of evil lurking within those funds. Plenty of investment products are not intended to be socially or environmentally responsible and are not at all represented as such. Indeed, the vast majority of investment funds reside at this end of the continuum. At the other end, rigorous responsibility focus exists in my mind as a sort of venerable ideal that is rarely, if ever, achieved. To be assigned a rating of 10 on my Responsible Investing Continuum, a fund and its management would need to

- skew strongly toward companies and industries making demonstrably positive contributions to society and the world;

- apply broad and strict negative (exclusionary) screening to block out any company substantially engaging in activities or behaviors injurious to the interests of relevant stakeholders (including climate and the environment);

- utilize an in-house research process to evaluate all companies and investment vehicles on a case-by-case basis according to a clearly defined, written assessment process and unambiguous responsibility criteria, while applying appropriate (ethics-, science-, and economics-based) judgment, and without undue reliance on external ratings providers; and

- practice ongoing, active engagement and stewardship in relation to portfolio companies and other issuers of securities held in the portfolio, possibly in collaboration with other portfolio investors.

These are, of course, very strict criteria. After all, ideal is ideal. I am presently aware of no publicly available collect investment vehicle that would earn 10 points on my scale.

Materials and methods

In order to do a high-level evaluation of an investment fund, you will need to obtain at minimum the following materials: a) a list of the fund’s complete holdings, and b) the fund’s current prospectus. Also useful may be the fund’s c) latest annual report, d) fact sheet, and e) possibly other materials such as an impact report or a standalone investment policy. All of these materials should be available (items in category c) if they exist at all) on the investment company’s website. In the U.S., by the way, every mutual fund registered with the U.S. Securities and Exchange Commission is required by law to disclose its full portfolio holdings on a quarterly basis.

As I have discussed at length in this and previous essays within this series, you, as a current or would-be responsible investor, will ideally have defined in advance what investments will and will not be acceptable for you, as well as how flexible you are willing to be on such criteria. So, if for example you are strictly unwilling to accept any investment in fossil fuel companies, then you can exclude a fund from consideration as soon as you see the first oil, gas, or coal company listed in the portfolio.

You will want to know what criteria and methods the investment company uses in selecting – and excluding – individual investments from the given fund. Some funds will use negative (exclusionary) screening to filter out all companies within specifically defined industries and sectors. Alternatively, the fund’s managers may use best-in-class selection, for example selecting the 20% most acceptable companies in any sector. In such case, of course, you’ll need to know upon what basis the 20% best companies are identified and how closely do those selection criteria align with your criteria. Of course, it is also possible to use exclusionary screening first and then apply best-in-class to what gets through the initial screen. The manager might also use a positive screening, thematic, or targeted approach that only allows companies from certain sectors and industries even to be considered for investment. That method, of course, will eliminate many companies from consideration, which makes investment decision-making easier but also reduces potential portfolio diversification. (One small note: In the ESG investment industry, the term “positive screening” is sometimes considered to be a synonym for best-in-class. I do not regard that as proper terminology.)

So far, this work has been pretty easy. Now things get a little trickier. The aim is to determine what is the research process that the investment managers actually pursue to determine whether a company gets into the portfolio or not and what sources of information do they utilize to achieve this. Ideally, they use all the information discussed above in looking at individual companies and much, much more. This might include a questionnaire to individual companies or even interviews with their managements. Commonly, however, it is based upon numerical scores provided by ratings agencies (such as CSRHUB or Sustainalytics, mentioned above). There may be no in-house research process whatsoever, or the methods might even be a black box wholly impenetrable to the clients. As the potential investor, you must decide whether the information available to you in this regard is or is not acceptable.

Finally, there is a question of active engagement and stewardship. This can range from just voting on shareholder resolutions at the annual meetings to applying direct pressure on company boards and managements to act in certain ways to, at the extreme, cooperating with other shareholders in efforts to force preferred responsible actions and behaviors. Stewardship is time-consuming and potentially costly. Moreover, unless a fund, or a family of funds under a give management company, has a holding large enough (or makes a big enough noise publicly) to get management’s attention, stewardship and engagement is probably not going to be very effective.

Six examples

By way of example, I will describe below six hypothetical investment funds and why they land where they do on my Responsible Investing Continuum. Each of them is typical of one or more collective investment offerings on the U.S. market.

Fiduciary’s Best (0 points) – This is a run-of-the-mill ex-U.S. investment fund, of which there are many in the market. It is invested in about 3 dozen companies in a dozen countries. The managers actively try to cherry-pick companies expected to bring superior returns, but Fiduciary’s Best has no CSR objectives whatsoever.

Holy Mary (1 point) – This is a faith-based (Catholic values) investment fund. It uses negative screening to exclude investments that could in any way involve abortion, embryonic stem cell research, family planning, or pornography. It nevertheless invests in weapons manufacturers, fossil fuels, and other potentially controversial sectors. Other than strict Roman Catholics, most responsible investors would not regard this as a CSR investment. Knowing that the Catholic Church does profess to care about the poor and certain marginalized people, I rate it with 1 point on the continuum (rather than 0). Some religious investors (or even others) might view this quite differently.

ISustain Index (2 points) – This is a low-cost, passively managed, exchange-traded index fund. Its investments consist of companies within the MSCI USA stock market index, a responsibility agnostic index encompassing about 85% of the total U.S. stock market capitalization and, in essence, not really different than the S&P 500. Starting from that list of 544 companies, however, the managers use a negative screen to exclude civilian firearms, controversial weapons, tobacco, thermal coal and oil sands, nothing else. Beyond that, it invests in the same stocks as are in its non-ESG benchmark index but does so while making what it describes as higher allocation to companies with favorable environmental, social, and governance (“ESG”) profiles. In determining those profiles, it discriminates only against companies directly involved in very severe, ongoing business controversies and considers only vital ESG issues that can lead to unexpected costs to the company itself in the medium to long term. The implication here, is that the interests of stakeholders other than shareholders are ignored or given low priority. My feeling is that this fund and its management approach are ESG in name more than in fact.

World Explorer (4 points) – This passively managed, exchange-traded international stock fund uses a rather coarse negative screen and a weak best-in-class selection process that is based upon a widely used ESG market index that is external from the investment firm. The index aims to exclude certain sectors, including all fossil fuels, certain weapons, tobacco and others, as well as companies not meeting certain human rights, corporate governance, and environmental standards. The CSR investment policy and management approach at World Explorer can be regarded as somewhat more substantive and rigorous renderings of those at ISustain Index.

Impact Leader (7 points) – This passively managed fund invests in most of the 360 stocks included in the MSCI KLD 400 Social ex-Fossil Fuels Index. That means it includes no companies that explore for, extract, refine, transmit, or generate electricity using fossil fuels (coal, gas, or oil). It excludes, as well, companies involved in alcohol, gambling, tobacco, military and civilian weapons, nuclear power, adult entertainment, and genetically modified organisms. The MSCI KLD index also uses a best-in-class approach to rating companies on ESG criteria and excludes the lowest-rated companies. This approach does let slip through some companies in industries that some investors will find objectionable (e.g., sugary drinks, fast fashion, vertically integrated U.S. health care providers), and it is very heavily weighted toward big tech companies that collect, process, and sell private data and are controversially building hundreds of massive data centers consuming enormous amounts of electrical energy and water.

Gaia’s Choice – In choosing its investments (totaling fewer than 100 companies), this actively managed fund does not attempt to match the composition of any index. It uses a negative screen to exclude investments in weapons and firearms, nuclear power, fossil fuels, for-profit prisons and immigration detention centers, alcohol, tobacco, and gambling. The portfolio nevertheless includes some companies that some investors would find objectionable. The fund’s management separates the ESG/sustainability screening process from the investment management process. That means an in-house team evaluates companies regarding responsible activities and behaviors (similar to my Stage 2 CSR screen) according to the management company’s own established policy and guidelines. A second team, then, runs the portfolio of investments into qualifying, acceptable companies. The fund’s managers commit to be actively engaged with managements of the portfolio companies, including by voting on shareholder resolutions at annual meetings, direct dialogue with management, and speaking out in cooperation with other responsibility-oriented investors.

Conclusions

So far in this essay series, I have provided a primer on responsible investing as a segment of the financial services industry, discussed the multidimensional challenges of pursing responsible investment, described how a would-be responsible investor can define and pursue one’s own views and preferences in responsible investing, and suggested how to build a basic level of investment knowledge to be a better responsible investor. In this essay, I have described example frameworks for screening out unacceptable companies and identifying acceptably responsible companies as potential investments and taking a discriminating approach to considering mutual or exchange-traded funds as responsible investment vehicles.

In my sixth and final essay, I will describe how I bring the responsibility, financial, strategic, and tactical aspects together in building and managing a responsible portfolio. Specifically, I will focus on analytical aspects of stock-picking. I hope you will join me. Meanwhile, if you have missed any of essays 1–4 in this series, now would be a good time to take a look back.

About the author: Gale A. Kirking is a Chartered Financial Analyst (CFA) and has earned the CFA Institute’s Certificate in ESG Investing. He formerly was employed as a senior equities analyst and director of investment research and has worked in and around the financial services sector for about 30 years. Kirking is not a licensed or registered financial adviser in any jurisdiction and does not make his living by providing financial advice. This essay and series are not intended to provide specific investment advice targeted or tailored to the needs of any individual investor. The views expressed herein are the opinions of the author. Other equally or more knowledgeable people will have different views.