By Gale A. Kirking, CFA

In previous essays, I have explained some of the challenges needing to be managed when a person wants to pursue socially and environmentally responsible investing, as well as how the investor can define one’s own views and goals in relation to responsible investing. Today, I’d like to discuss acquiring a requisite base of knowledge about financial markets, investment instruments, and investing generally in order to be able to design, build, and manage a responsible portfolio. The level of investment know-how one needs will range from the very basic if a person has hired highly qualified advisers to assist in creating and running his or her investment portfolio to the very sophisticated if one is himself or herself a professional investor with responsibility for other people’s money. The average, or typical, responsible investor, it seems to me, will find oneself about in the middle of this range.

With luck (and enough money to invest), you may find a knowledgeable, experienced, competent, and scrupulous professional to assist you in constructing your responsible portfolio. To any extent that is not your case, you need to learn how to do it by yourself or possibly in cooperation with like-minded others.

With a view to acquiring this essential know-how, I will address its financial aspects in this essay and the social and environmental responsibility aspects in the following essay. For a person solely motivated to achieve the highest possible money returns, only the financial aspects will be of interest. For somebody who has some degree of responsibility concerns (maybe a little, maybe a lot), then knowledge in both areas is important. Although the two subject areas should, to a certain extent, at least, be understood in an integrated manner, I personally try to separate them as much as possible. I like to make what I call the corporate social responsibility, or CSR, decision a binomial one: either, yes, I am interested in investing in this stock, or no, this company does not meet my responsibility criteria and I will not purchase its shares. I will have more to say about this in my next essay, and the fact of the matter is that the answer to what I term this “CSR question” is sometimes neither “yes” nor “no” but instead “maybe.”

Financial and investment know-how

For me investing is an enjoyable intellectual pursuit, and I think that’s pretty common among active investors. An active investor needs to acquire a certain level of know-how to get started and thereafter learning should be continuous. Although luck, intuition, and general cleverness are all nice-to-haves when investing, we cannot count upon these to carry us to investment success. In addition to a base of knowledge, by the way, discipline, self-understanding, and meticulous attention to detail also are essential elements. Humility, too, is enormously helpful.

I won’t try to provide a course on investment management here, but I would like to introduce a few financial and investment concepts that an investor should learn about as much as reasonably possible and over time. By the way, if you consult my Substack (https://galekirking.substack.com/), BlueGreen, you will find there a growing series of book reviews where I introduce and discuss those books which have been most valuable to me through the years in learning about investment.

In particular, I will discuss briefly in this essay 1) what are financial instruments and a portfolio, 2) four determinants of investment portfolio performance, 3) the passive–active management continuum, 4) various views concerning what is risk and how to manage it, and 5) the area of investment costs. I will then introduce four possible approaches one might consider in setting up and running a responsible portfolio.

Financial instruments and a portfolio

Every investor whose money is put to work in more than one place or in more than one way can be said to have an investment portfolio. Among other investment instruments, a portfolio can include bank accounts and deposits, stocks and bonds, investment real estate, insurance policies, as well as so-called alternative investment products, such as private equity or venture capital partnerships or hedge funds. For simplicity’s sake, and as I have been doing throughout this series of essays, I will speak here especially of common stocks, also known as equities, and to a certain extent about collective investment instruments.

Let’s take a particular person as an example. I’ll call her Sally. Sally’s financial life is fairly simple. She has a checking and savings account at her credit union. She bought a certificate of deposit (CD) at the credit union several years ago and she keeps letting it roll over. She also has a money market account at her credit union. Sally owns the condominium where she lives but still has 18 years to pay down the remaining 65% of her mortgage. Recently, she opened a brokerage account with Vanguard, the client-owned financial services company, where she put $3,000 into a low-cost, no-load index fund that tracks the S&P 500 stock index, and she committed herself automatically each month to send $50 to that fund. She set up that account as a tax advantageous individual retirement account (IRA).

Click on a link below to read this

and Kirking’s first three responsible investment essays

on Channel BlueGreen (https://bluergreener.world/blog/)

or at Substack (https://galekirking.substack.com/).

Sally’s investment portfolio consists of her bank accounts, CD, the equity in her home, and her IRA index fund. Each of her holdings bears particular risks and offers certain expected returns. We say that each has its own “risk–return profile.” To certain extents, the risks and expected returns of these portfolio constituents offset and balance one another. Sally will be wise to look at those risks, returns, and other characteristics (especially liquidity, which is the ease and rapidity with which an asset can be converted to cash) collectively, which is known as taking a “portfolio view” of these.

The expected returns and risks on all of Sally’s assets may not be explicitly quantifiable, but that doesn’t mean they aren’t there. For example, Sally does not anticipate getting big returns on her savings account, but it is federally insured and she can be pretty confident that her money isn’t going to disappear. The main risk to those funds is that they will shrink in real terms because the interest rate they earn is much lower than the inflation rate. Meanwhile, she perhaps has already seen the value of her index fund fall below the $3,000 she initially put into it but it always has bounced back into positive-return territory and she expects to get good earnings that are well in excess of inflation over the period of three or four decades that she plans to leave that money there. So, the index fund is risky in the near term, not so risky in the long term.

Can Sally make her portfolio socially responsible? Yes, she can, and especially as it continues to grow. For example, she can add ESG-oriented mutual funds or exchange-traded funds (ETFs) to her IRA account. She might even add individual stocks and bonds of companies that she deems socially responsible. I will say more on that in my next couple essays.

Four determinants of investment portfolio performance

In creating and managing an investment portfolio, there are four overriding ways for the investor potentially to influence returns, as well as risks. These I will term 1) asset allocation, 2) securities selection, 3) market timing, and 4) pricing execution. These four also reflect major decision points in the investment process.

Asset allocation

Investment assets can be grouped into various classes and in different ways. For example, Sally’s portfolio includes bank accounts (checking, savings, certificate of deposit, money market), an owned albeit mortgaged home, and a stock index fund. These assets can be classified, respectively, as cash, real estate, and equities. Each of these has a different risk–return profile.

Thinking strictly in terms of marketable securities (i.e., stocks and bonds), many investors are familiar with the traditional 60:40 asset allocation, often referred to as a “balanced” portfolio allocation. That means they are advised or otherwise decide to have a securities portfolio that is 60% invested into stocks and 40% into bonds. This is sort of a default asset allocation, a general guideline, but it’s not the right mix for all people at all times. Depending upon one’s stage in life, risk preferences, current market conditions, other investments held, and additional factors, an investor’s optimal securities portfolio could differ slightly or greatly from this 60:40 asset allocation.

Stocks, bonds, real estate, and cash are high-level “classes” of assets, and asset allocation is the set of decisions determining how much of one’s funds should go into each class. In fact, however, each of these (and other) classes can be further subdivided into what we might call subclasses.

For example, stocks are subclassified as large capitalization and small capitalization (so-called “large caps” and “small caps”), “growth” versus “value” versus “income,” as well as international (the latter itself subdivided into developed market and emerging market). Then, too, there are stock themes, such as health care, water, energy, and technology, as well as subsectors, like consumer durable goods, consumer discretionary, and industrials. Some might consider ESG to be a class or a theme, but I would not.

Bonds make up the main proportion of the broad asset class known as fixed income, and this includes asset-backed securities, U.S. Treasury bonds, municipal bonds, corporate bonds (including junk bonds, convertible bonds, zero-coupon bonds, among others), preferred shares, and many other types of investment instruments.

Then, too, there are so-called “alternative” investment classes, like hedge funds, private equity or venture capital partnerships. Some people regard real estate as an alternative investment, but it is an asset class in any case and includes several subclasses, such as, for instance, one’s own residence, various types of commercial buildings, residential rental properties, farm and forest land, and others.

Most financial professionals and academic experts in the field agree that asset allocation is the main determinant of long-term portfolio returns, that stocks bear greater risk than do bonds but have higher expected returns in the long run, and that while middle-class savers might want a little exposure to alternative investments these are mostly for rich people who can bear greater risk of loss. Most agree, too, that real estate in the form of owning one’s residence is about the best asset allocation of all.

Securities selection

Within each of the various asset classes, the investor can select from a range of possible investment vehicles. For example, the S&P 500 index is made up of 500 large companies. If a person chooses to invest into the shares of all 500 companies through an index fund, then he or she has not really engaged in securities selection. But, if that investor chooses to buy 3 or 4 or even 20 or 30 of these 500 that she thinks will outperform the others or that she prefers for some other reason, then the investor has done securities selection. By the way, proponents of the so-called “efficient-market hypothesis,” or “EMH,” think that an investor is just as likely to win on performance by drawing those company names out of a hat as to studying the individual stocks. EMH diehards don’t believe in securities selection. Fair enough, because active securities-selecting investor diehards don’t believe in EMH either.

In the fixed-income market, too, each asset subclass has a more or less broad choice of individual securities from which one can choose. For example, should I buy a corporate bond issued by Harley-Davidson that pays a coupon of 3.50% and matures (i.e., the principle gets paid back) in 2 years or a bond from American Airlines with a 4.00% coupon maturing in 5 years? If I’m buying a municipal bond, should I select a so-called “general obligation” bond financing a school in Detroit, for example, or a “revenue bond” issued to build a nursing home in rural Arkansas?

Although I’m using the term “securities selection,” the same concept is important for other asset classes, too. For example, Sally bought a condominium in a nice neighborhood largely populated by young professionals and not too far from a city’s downtown, but she might have chosen to buy a small house in the suburbs or an old farmhouse with 2 acres in the countryside. Each of these has its own risk, return, and liquidity characteristics.

So far as the stock market is concerned, and assuming that good diversification is maintained, many (but by no means all) experts agree that securities selection is a less important determinant of investment returns and risks than is asset allocation because

1) all stock prices tend to go up and down together, following the general market; and

2) stocks of poorer quality companies will trade at lower prices and stocks of higher quality companies at higher prices, the only way to beat the market is to buy a stock that is underpriced relative to its quality or to sell one that is overpriced relative to its quality, and almost nobody is smart enough to determine when a stock is underpriced or overpriced anyway.

There are a good many active investors, too, who do not subscribe to the view I have described just above. Some people think that “stock-picking” (another term for securities selection) is just about the most important thing of all when it comes to achieving outstanding returns.

Market timing

The third determinant of investment portfolio performance is market timing. We most generally think of this in stock market terms as buying stocks when the overall market is cheap and selling out when the market gets overheated but before the bubble bursts. Many investors get this almost perfectly wrong, by the way, buying in when euphoria has driven market prices to unsustainable highs, selling out at a loss when stock prices disappointingly fall or are stuck in the doldrums, and then sitting it out when the market has already bottomed only to miss the next move upward.

Will Rogers, the early 20th century American humorist, is famously said to have advised, “Don’t gamble! Take all your savings and buy some good stock and hold it till it goes up, then sell it.” And if it doesn’t go up? he’d be asked, “Then don’t buy it,” he’d quip.

Most experts (and comedians) probably agree that market timing (i.e., attempting to buy at market lows and sell at market highs) is a fool’s game. From my personal observation, yes, that is probably true but there is a pecking order of fools. I think that what I call “smart money” continues to buy when the market is rising unjustifiably and is standing ready to sell (“looking over their shoulders,” as I like to say) near the market top when the last possible fools have finally put their money into the surging market. As evidence of this, market peaks tend to be followed by sharp selloffs, as the smart money people flee with much of the last fools’ money in their bank accounts.

Of course, market timing also applies to other asset classes. In real estate, for example, this might work out better for people clever enough to understand local market supply and demand, the effect of interest rates, general economic growth, and so forth.

At the time Sally bought her condo, let’s say she judged that residential real estate prices were pretty reasonable locally because there happened to be a good supply of condominiums, as several new developments were just being completed even as demand was a bit stifled because one big local employer had just announced that it was downsizing its staff. Interest rates were a little high, but she’d read that rates should be coming down over the next year and that that would help housing prices to grow. Now was the time to buy, she had decided, and she decided right. She had good market timing.

Pricing execution

Finally, let’s look at what I’ll call pricing execution but also might be called just “pricing” or even simply “buying and selling.” I think that most successful active investors will tell us something to the effect that “price always matters.” If you pay too much for a stock, your future returns will be smaller and you might even be in a losing position from day 1. But if you buy at a bargain price, your future gains will be greater. Like market timing, this, too, is about “buy low, sell high,” but it differs from timing inasmuch as this concerns buying or selling an individual stock at any given moment in an actively moving market at a price that is momentarily advantageous relative to the “actual value” of that stock. I put that in quotes, because “actual value” is a nebulous and squishy thing.

So-called “value” investors, and most famously Warren Buffet, speak of buying a stock at a price lower than its “intrinsic value” while building in a “margin of safety” by doing so. Let’s say Mr. Buffet thinks the shares of Kroger, the big U.S. grocery store chain, are worth $50. Now, that is his informed opinion, but he knows that the stock might also be worth $45 (10% less). He’s going to wait patiently until the share price falls to $40 (20% less). That 20% is his margin of safety.

Now, most investors will have neither an informed opinion as to the intrinsic value of the Kroger shares nor the patience to wait for the price to fall by 20% for a stock they want to buy. Selling when a stock is overvalued can be even more tricky. Who wants to sell Kroger at $50 (when fully valued in Mr. Buffet’s current view) or even $60 when it might go to $70 or $80?

Instead of thinking about intrinsic values and being disciplined, some people feel they can outsmart the market by buying low and selling high according to their gut feelings. We call these people speculators, not investors.

Of course, theory is one thing but reality can be quite another. If a person wants always to be fully invested in the stock market, then it may be difficult sometimes to buy at attractive prices when, for example, a stock market bubble is inflating.

Wrapping up

In summary, most investment advisers will tell their clients that asset allocation is the most important determinant of investment outcomes. Individual securities selection based on financial criteria may not pay off for most investors, and not even for many professional investors. Securities selection based on social responsibility criteria is another matter, and I’ll talk about that in my next essay. Market timing is a fool’s game. Sally has decided not to play that game. With her index fund, she uses what is called “dollar-cost averaging.” She puts $50 into the market on the same day every month, whether share prices are high, low, or somewhere in between. On average over the long term, therefore, her dollars will grow at the rate that the overall market appreciates. Attempting to buy low and sell high in the stock market is really tough to do well. It takes a lot of time to develop a studied view on intrinsic value for every stock in, or potentially in, one’s stock portfolio and both time and discipline to actually execute superior purchases and sales relative to that view.

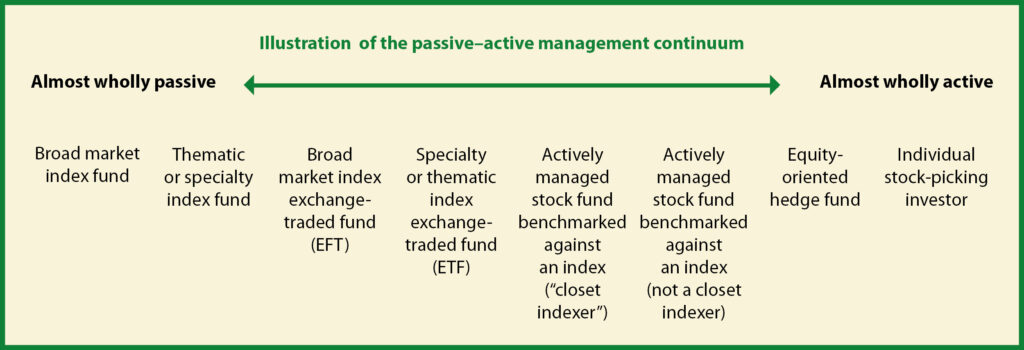

The passive–active management continuum

In 1976, Vanguard Group launched its Vanguard 500 Index Fund, the first investment instrument of its kind to become a major force in the investment market. This was the initial shot setting off a revolution in passive investing. That index fund essentially mimicked the S&P 500 index that includes approximately 500 of the largest publicly traded companies in the U.S. stock market. By purchasing a share in this mutual fund, an investor essentially obtains a size-weighted ownership interest in every company within the index at the current market price of each company’s shares. This involves no analysis as to which stocks are overpriced or underpriced, which are safe investments or risky investments. The costs of running an index fund are low, and Vanguard passes the resulting savings on to the shareholders in such funds, which, uniquely in Vanguard’s case, also happen to be the owners of the management company.

Soon, Vanguard’s competitors had little choice but to launch index funds of their own, because the low costs associated with operating a fund that simply mimicked the market trumped any possible superior investment returns that other, actively managed, investment funds might achieve through extensive research and analysis, security selection, and careful buying and selling. Indeed, most active funds found they couldn’t achieve returns superior to those of the passive index fund even before considering the costs that they would charge to the clients.

Although the shares of the 500 largest companies in the U.S. already constitute approximately 80% of the total U.S. stock market, in 1992 Vanguard went a step further, introducing its Total Stock Market Index Fund, which today embraces more than 3,500 companies and essentially allows the fund shareholder to own thousands of teeny tiny bits of the whole U.S. stock market. There exist today many competing market index funds and about half of all the billions of U.S. shares that companies have issued and sold into the market are passively managed.

Simply put, passive management – or passive investing – means buying and sometimes selling stocks (or bonds) while giving little or no thought to what one is buying or selling. Active management, by contrast, involves research and analysis, securities selection, and attention to pricing execution.

In practice, there exists a range of investment approaches spanning between almost purely passive and almost entirely active. The figure below uses examples to illustrate this continuum.

A broad market index fund (far left on the continuum), like the Vanguard 500 mutual fund into which Sally has invested, is almost wholly passive. The only really active thing the folks at Vanguard have done is to choose which companies will be included into the index and which ones will not, and even that is pretty much decided by default. From Sally’s viewpoint, she’s not even going to know what are the 500 companies in that index. (By the way, as I wrote in my first essay in this series, that index is what I call “socially and environmentally agnostic.” It doesn’t make any value judgments about whether the constituent companies are responsible, irresponsible, or somewhere in between.)

At far right on the pictured continuum, we can imagine an individual investor who spends her free time doing research and analysis of individual companies in order to pick individual stocks, then buying and sometimes selling these with the aim of beating the market and/or potentially to achieve some other objective, such as to maximize social responsibility. That’s where I am, for example. My personal aim is to achieve what I call “superior socially responsible, risk-adjusted return” through a thematic investment approach. I will describe that in my next essay.

I’ll just mention a few other points on the continuum from left to right. The thematic or specialty index fund is one that encompasses not the whole stock market but a particular more or less narrow part of it. I call this less passive because the investor must choose on the basis of some hopefully informed view to put her money to work in that specific area to the exclusion of others. Moreover, whoever dreamed up the particular fund had to decide what to include and not include into the index. Further to the right, I place the exchanged-traded funds. These are in principle passive, being based on an index like a mutual fund. The difference is that, whereas a mutual fund is usually treated as a “buy and hold” investment, the ETFs can be bought and sold on the stock market on a daily basis. ETFs are in fact used pretty often for speculative purposes, which is good for their creators in the financial services industry, as this generates for them fees and commissions. Arguably, this is not so good for the speculators in the same sense that Mom or Dad going to the casino on Friday nights is probably not supportive of the family budget.

A bit further to the right, some professionally managed investment funds are said to be actively managed, with the managers, doing research to pick out the best investment opportunities, even though those managers are in fact “closet indexers.” If the benchmark to which such a manager’s performance is compared happens to be the S&P 500, for example, then the manager’s investment picks may not much differ from the stocks that are in the index. While it is nice to beat one’s benchmark once in a while, a closet-indexing professional wants to avoid the career risk of potentially ever being trounced by that benchmark.

Views on risk

Speaking of risk, this is an aspect of investing that everybody talks about, many don’t understand very well, and in actual investment practice probably gets less attention than it deserves. We’ve all heard things said like, “If you want to achieve high returns, then you have to take big risks.” This is not strictly true, by the way. Many risky investments simply have much higher probability of going bust than they do of achieving enormous returns. Also, investment returns are much more exciting to dream and talk about than are risks. We are more likely to hear at a cocktail party that somebody achieved 1,000% return on his NVIDIA shares than that he invested in a startup company that he’d read about on Reddit and which ended in bankruptcy.

Diversification is the major means that investors use to manage risk. They invest in various asset classes and “don’t put all their eggs in one basket,” as the wise saying goes. Sage investors are careful not to be overly exposed to any particular business or economic segment. If one is employed by a company supplying components to the auto industry, for example, it might not be the best idea to have a large part of his or her stock portfolio invested in Ford and General Motors.

In terms of financial theory and the stock market, we speak of “systematic” versus “unsystematic” risk. Systematic risk, also known as “market risk” is inherent to the entire stock market and cannot be diminished through diversification. For example, economic growth, inflation, interest rates, and currency exchange rates are systematic risks and tend to affect the whole market about equally. Unsystematic risks are specific to individual firms and so investing in a range of very different companies can reduce the unsystematic risk of one’s overall portfolio.

Finance professors tend to associate stock price volatility with risk. They use statistical measures of how much stock prices are going up and down, and especially of the standard deviation from the index or share price mean. They like to come up with numbers to specify risk. Many smart investors, though, say that volatility is a poor measure of risk and that risk is too complicated to be expressed as a number. They may say that the risk of losing the originally invested amount is the only or main risk that really matters. They call it “permanent loss of capital.” It’s hard to argue with that. If you invest $1,000 in a stock position and the market value goes up and down, say in a range of $800 to $1,200, you’re probably doing okay, but if the value falls to $0, well, that’s game over for that investment.

From a permanent loss of capital perspective, then, the main thing is to not invest in anything that has even a remote chance that its value will fall to zero.

In my forthcoming sixth essay in this series, I will write a lot more about risk, but I’ll just note here that it’s probably not a very smart idea to make risky investments with the anticipation that they are going to lead quickly to a place of boundless riches. One of my favorite professional investors and investment authors, Howard Marks, writes more about risk than probably any other investment author I’ve ever read. In fact, I think he writes more about risk than he does about investment return. At his company, Marks relates, “we believe firmly that if we avoid the losers the winners will take care of themselves.”

“I don’t think many investment managers’ careers end because they fail to hit home runs,” Marks adds. “Rather, they end up out of the game because they strike out too often – not because they don’t have enough winners, but because they have too many losers. (See my review of Marks’ book The Most Important Thing at my Substack, BlueGreen: https://substack.com/@galekirking/note/c-167305548).

Costs and fees

As alluded to earlier, one of the main reasons for the success of Vanguard and indexing is the emphasis on low costs and fees. Once the technology is in place to manage an index fund and millions or billions are under management, it costs almost nothing (in relative terms) to manage those assets. Moreover, because Vanguard is essentially owned by the same people who invest into its funds, this truly mutualized mutual fund provider needn’t generate profits for its shareholders. This is not to promote Vanguard, but I am writing this to illustrate a point: The costs and fees of your investment adviser, broker, or fund manager invariably come out of your investment returns. So, costs matter – a lot.

It used to be, not so many years ago, that the stockbroker would take a standard 8.5% front-end load (also called a “sales fee”) on every new mutual fund investment a customer would make. That means that if one gives the broker $1,000, then $850 of it is invested and $150 goes, well, elsewhere. The investor is already down 8.5% and the game hasn’t even started yet.

By law in the United States, sales fees cannot exceed 8.5% today, and few mutual fund managers would actually try to extract such exorbitant amounts, but loads in the range of 3% to 6% are still pretty common. Also, brokers and advisers may adjust these according to how much a person has to invest and how much advice he or she expects to receive. More money to invest and less need for advice should equate with lower fees. Many investors these days (myself included) refuse to pay any front-end loads, but we don’t get any expert advice, either.

Because investment advisory is not generally provided as a charitable activity, if one hires an adviser the investor must expect to pay for the service. Instead of paying front-end loads and other fees to cover the costs of advice, some investors and their advisers agree to a so-called “wrap fee” (typically around 1% of assets per year) to cover the costs of advice and other services.

There are many kinds of fees and costs. In addition to front-end loads, some mutual funds have back-end loads, paid when the investor sells the investment. There are also 12b-1 fees, which mutual funds charge their current clients in order to pay for advertising to attract new clients. Then there are management fees, which are what a mutual fund charges investors for the service of running the fund. In buying and selling individual securities, investors sometimes pay commissions to the brokerage. This always used to be the case, by the way, because that was the only honest way for a broker to make money on that activity.

These days, in the U.S., investment fund managers are required by law to report “Total Annual Fund Operating Expense,” which includes any of the fees and costs I’ve mentioned above, as well as any others they charge to the client. The main point to remember is that fees matter, because they come directly out of investors’ returns or, in a bad year, are added to their losses. The U.S. Securities and Exchange Commission’s Office of Investor Education and Advocacy has an excellent Investor Bulletin on this subject entitled “How Fees and Expenses Affect Your Investment Portfolio.” I recommend it. Just in case that brochure were to disappear from the federal website, please feel free to contact me and I’ll send you a copy by email.

Four general approaches to socially responsible investment

Learning about financial markets and investment can be a never-ending journey, and the surest way to educate oneself is eventually to set out on that adventure. In my next essay, I will come back to the possible social and environmental responsibility aspects of this excursion, which is, of course, the raison d’être for this whole series, but I’d like to end today by generalizing four possible approaches to such investing.

1) Collective investment on your own

Perhaps the easiest approach to responsible investing (as well as responsibility-agnostic investing) is to buy collective investment vehicles, typically mutual funds. The investor should do well to choose a reputable, low-cost online broker or investment company (and these two terms are nearly synonymous these days), set up an investment account (quite possibly as an IRA if you live in the United States), then pick several collective investment vehicles (probably mutual funds, maybe exchange-traded funds). Advisers often suggest that individuals spread their stock investments over at least four or five different asset subclasses, such as, among other possibilities, large caps, small caps, mid-caps, international stocks, value stocks, and possibly a specialty fund or two of some sort. Most people will pick index (passive) versions for some or all of these subclass choices as opposed to buying only actively managed funds. These days, it is generally possible also to find versions of almost all the above being marketed as “ESG,” “sustainable,” “responsible,” or something of that sort.

For the would-be socially and/or environmentally responsible investor, this approach may demand that you compromise somewhat on your moral preferences and principles. If you don’t look too closely at the particular funds you’re investing in, you won’t know just how egregious are your compromises. Most such funds either will take a best-in-class stock selection approach and/or will use a high-level screen (termed “negative screening”) to exclude the most objectionable companies. I wrote about best-in-class investing in my second essay in this series and explained how this can let in companies that many responsible investors will in fact find objectionable. The negative screening approach, too, may let some potentially offensive investments slip through.

Despite its shortcomings from a responsibility viewpoint, I think this collective investing on your own is a very good way to get started in responsible investing. It’s relatively easy and needn’t cost much in terms of fees. In fact, the investor might choose to direct only part of his or her investments to “ESG” or similarly identified funds. As you gain experience, learn more, and have additional money to invest in the future, you can always get more sophisticated and fastidious in your investment choices. Important, I believe, is for the investor to read the prospectus and other information materials for each investment fund, and especially to look at the investment objective, investment strategy, securities selection, and proxy voting policies that are in each individual fund’s prospectus and in the document termed the “statement of additional information.” The investor also will want to review the complete list of each fund’s portfolio holdings, which every publicly offered mutual fund in the United States must provide. You may or may not completely like what you see there, but at least you’ll be acting with fullish information.

2) Use a fee-based adviser

There are a lot of people “out there,” as we might say, representing themselves as financial advisers, and, as a general matter, they are not hard to find. Indeed, they might very well already have found you. Depending upon what country you live in and other factors, these people can range from complete shysters and ignoramuses to highly trained and experienced professionals. In most U.S. states, I think this is fairly well regulated these days on both the state and federal levels, and those presenting themselves as advisers should be able to show that they have earned and hold certain licenses and qualifications. For example, a Series 6 license is required to sell mutual funds and certain other packaged securities, a Series 7 is mandatory to sell most all other types of securities, and a Series 63 qualifies one to give broader financial advice.

In addition, there are professional certifications that advisers earn above and beyond the basic licenses. For example, a Certified Financial Planner (CFP) has comprehensive training in financial and retirement planning and general investment management. A Chartered Financial Analyst (CFA), the professional designation I have, is focused especially upon securities and investment analysis, portfolio management, and professional ethics. The CFA Institute also awards a Certificate in ESG Investing, which again, by the way, is a designation I have earned.

Not all financial advisers are the same

Ideally, if one is to hire an adviser to help in constructing and managing a responsible portfolio, he or she would want that person to be knowledgeable about a) analyzing individual companies, securities, and other investment vehicles as good investments; and b) specifically evaluating potential investments in terms of their responsibility (ESG, sustainability) characteristics. Many good advisers are able, as well, to offer a much broader palette of financial advice in areas like c) insurance, mortgages, tax strategies, estate planning, and even much more.

Some advisors are good at a) and c). My guess is that rather few are really good at a), b), and c). I discussed the reasons for this at considerable length in my second essay within this series. You may recall the hypothetical situation I described there wherein would-be responsible investors Ted and Mary were having difficulty getting good and straight advice on responsible investing that would correspond to their own views and preferences from John, their professional investment advisor.

First of all, John and the firm within which he worked were very much concerned about fiduciary duty, which may not accord real well with the clients’ responsible-investing interests. Then, too, John had a fairly limited selection of less-than-ideal responsible investment instruments that he could offer. Moreover, the 1% wrap fee that John was charging Ted and Mary was not enough to justify his spending hours and days searching for individual stocks and bonds that would suit the couple’s preferences. In any case, John was not trained, experienced, and qualified either to pick individual stocks and bonds or to advise in details on responsible investing. Of the three knowledge areas cited in the previous paragraph, John is really good at c) the broad palate of advisory services; he has certain limitations in a) analyzing individual investments; and he is neither very competent nor motivated to excel in b) advising on ESG and the like.

So, if responsible investing is your aim, and you plan to depend upon an advisor to help you with this, then you need to determine in advance which skill set you’ll be getting from whom. For some people, it might make sense to hire a second adviser to focus just on the responsibility aspects of choosing investments, but that will mean more fees, and so that’s probably just for high-net-worth investors. Moreover, the primary adviser may not be very amenable to bringing a second advisory cook into the kitchen.

3) Join or create an investment club or group

Investment clubs, as I recall, were pretty popular in the 1980s and 1990s. Together with a bunch of other expatriates, I belonged to a rather informal one in Prague at the time that the Prague Stock Exchange was reemerging after two decades of communism around 1993. I suspect that the investment club concept largely fell out of favor after the 1998 financial crisis and was finished off by the 2008 financial crisis. That’s too bad. These days, a lot of ideas exchange has of course moved online, but that’s just not the same as a bunch of friends sitting together periodically, eating pizza, and listening to one another present their investment ideas.

The most famous investment club of all time must surely be the Beardstown Ladies Investment Club, which was founded in the 1980s by 16 women meeting in a church basement in Beardstown, Illinois. Amazingly, perhaps, as of last year, two of the charter members were still living, the club was still limited to 16 members, and the members were still putting $25 a month into their collective investment, as had long been the custom. The two remaining charter members were interviewed on National Public Radio in Illinois in spring of 2024.

In some cases, an investment club may need to register (in the U.S.) under state and/or federal law (See: Investment Clubs and the SEC.), but I’d personally like to advocate for a more informal approach whereby the members of a group do not necessarily pool their assets into a single portfolio but rather make their own investment decisions about their personal portfolios while sharing ideas.

Formal or informal, pooled or not pooled, an investment club has the advantages of bringing together various professional talents and perspectives. So, some members might be strong on financial analysis, others on social and environmental scrutiny, and still others on understanding specific industries.

4) Go it alone

A fourth approach is to go it alone – personally to analyze individual companies and other securities issuers, buying (and sometimes selling) on one’s own, quite possibly while including also some mutual or exchange-traded funds into the personal portfolio. Researching and analyzing companies and other potential investments can be a fascinating intellectual activity, and even more so when considering social and environmental responsibility aspects. There is a lot to wrap one’s brain around, and so it can be pretty time-consuming, too. I sometimes say that if buying mutual funds is checkers and active investment is chess, then active responsible investment is three-dimensional chess.

I will share a few tips here about going it alone that are based upon my own experience, but I will have much more to say on this subject in the sixth and final segment of this series.

Most importantly: Do not get into day trading. No matter what anyone tells you, buying and selling on Robinhood or any other such trading platform is a bad idea. If you do so, you will lose money and instead of making a contribution to society through responsible investing you will make an involuntary donation through speculation to an online broker with whom you will have a relationship only until you go bust or lose all nerve. The vast majority of people who try this greatly underperform the broader markets and even lose money. That is a fact, period. Robinhood does not steal from the rich and give to the poor.

As I have described above, in order to be successful, personal active investment requires time for the work involved, patience in order to avoid getting out ahead of one’s capabilities, a reasonable level of financial and investment knowledge, and experience that only can be accumulated with time in the market. That means a new active investor should start out slow. Research one stock (or possibly a bond or mutual fund), then work on another. Be prepared to discard 9 out of 10 investment ideas that you begin to study. Do the research first, then invest, keep following and learning about each company that you invest in, and, as you gain conviction in your decision, add to your position. I recommend you at first limit your research to a sector or two you understand. Nobody can learn the whole market.

Diversify absolutely, but also very important is to know what you’re invested in. And by the way, if you study the responsibility aspects, you can know a company much more comprehensively than you would just from looking at the financial statements. In my opinion, it is better gradually to invest into maybe 8 or 10 companies that you know well while holding the rest of your investable money in a money market mutual fund than to be invested quickly into 20 or 30 or more individual companies that you don’t understand.

Write things down and keep a record of what you are doing and why. I strongly recommend that a new active investor formulate a simple policy and/or strategy that you can stick to. Then write it down and use that written statement to ground your own discipline. For example, one might formulate something like the following:

My investment strategy

(an example)

I will start out slowly. I will put $10,000 into my IRA account’s interest-bearing money market fund, and I will draw from that money to buy individual stocks in companies that I believe are socially responsible and can yield good investment returns over the long term. My initial investment in any particular stock will be not more than about $1,000. I can always add to my position later as my conviction in that investment grows.

I will invest in no stock of an individual company until I have thoroughly studied that company. I will examine its business, market and competitive position, and financial situation. I will understand the profitability, risks, and earnings growth potential of the company before investing. Because I want to be a responsible investor, I also will examine the environmental, social, and governance strengths and weaknesses of the company before investing.

I will seek to buy stocks that are fairly valued or undervalued by the market relative to what I believe are their intrinsic value. I will avoid high-flying companies whose stocks are selling at very high valuations as measured by price/earnings ratios and price/book value ratios.

I only will buy the stocks of companies that I believe I will be able and want to hold for the long term. I will make no investment that could keep me awake at night. At least 70% of my individual stock portfolio will be a core portfolio of conservative, dividend-paying stocks in companies with strong balance sheets (i.e., low debt, plentiful cash, and minimal intangible assets), with long histories of profitability and continuously growing dividend payouts. A smaller proportion of my stocks – the “extended portfolio” – may consist in stocks of newer companies with excellent growth potential but somewhat higher risk.

I will regard investment risk first and foremost to be the potential for permanent loss of my investment capital.

Another aspect of writing things down is to keep permanent notes while you are analyzing companies for potential investment. I have a separate “research” subdirectory on my computer for every company that is in my portfolio and for every one that is on my watch list of companies potentially of interest. I also keep research subdirectories for companies that I once thought looked interesting, began to analyze, and then rejected. In each of these subdirectories, I collect annual reports, ESG reports, company press releases, and other materials specific to that company. Most important, though, I have an MS Word file where I keep notes on that company. I write down my observations, my analyses, my investment thesis (more on that in my upcoming part six in this series) and my CSR case (more on that in part five). I never delete anything I write in my Word file. Rather, I just let the document grow in length while adding new and specifically dated notes at the top.

Because of my MS Word file for each researched company, I can look back and see why I did – or did not – invest in a specific company in the past. I can see what were my investment thesis and CSR case for a company whose shares are in the portfolio. You will be surprised how easily one can forget why he or she bought a particular company’s stock in the first place. I can ask myself months or even years later whether my original investment thesis on a company still holds. I also can see if the reasons I rejected a company as an investment still exist.

And one final tip before leaving this section: Never buy anything on the basis of advice and “hot tips,” whether from friends, strangers, media personalities, or “news” stories. This advice applies also to professionals unless you have specifically hired them to provide you buying advice. There’s an old joke in the investment business that asks, “How can you tell if your stockbroker is lying to you?” Answer: “You can see his lips move.” There’s another one about the investment adviser who is showing off his yacht and who is asked “Where are the clients’ yachts?”

5) A hybrid approach incorporating some or all of the above

I promised four general approaches to socially responsible investment, but let me close by adding one more, perhaps very obvious, possibility. There is no reason why an individual investor cannot or should not combine aspects from all four of the general approaches that I have described above. There are a lot of ways to invest, and, as Mark Twain said about horse races, it is differences of opinion that make a market.

About the author: Gale A. Kirking is a Chartered Financial Analyst (CFA) and has earned the CFA Institute’s Certificate in ESG Investing. He formerly was employed as a senior equities analyst and director of investment research and has worked in and around the financial services sector for about 30 years. Kirking is not a licensed or registered financial adviser in any jurisdiction and does not make his living by providing financial advice. This essay and series are not intended to provide specific investment advice targeted or tailored to the needs of any individual investor. The views expressed herein are the opinions of the author. Other equally or more knowledgeable people will have different views.